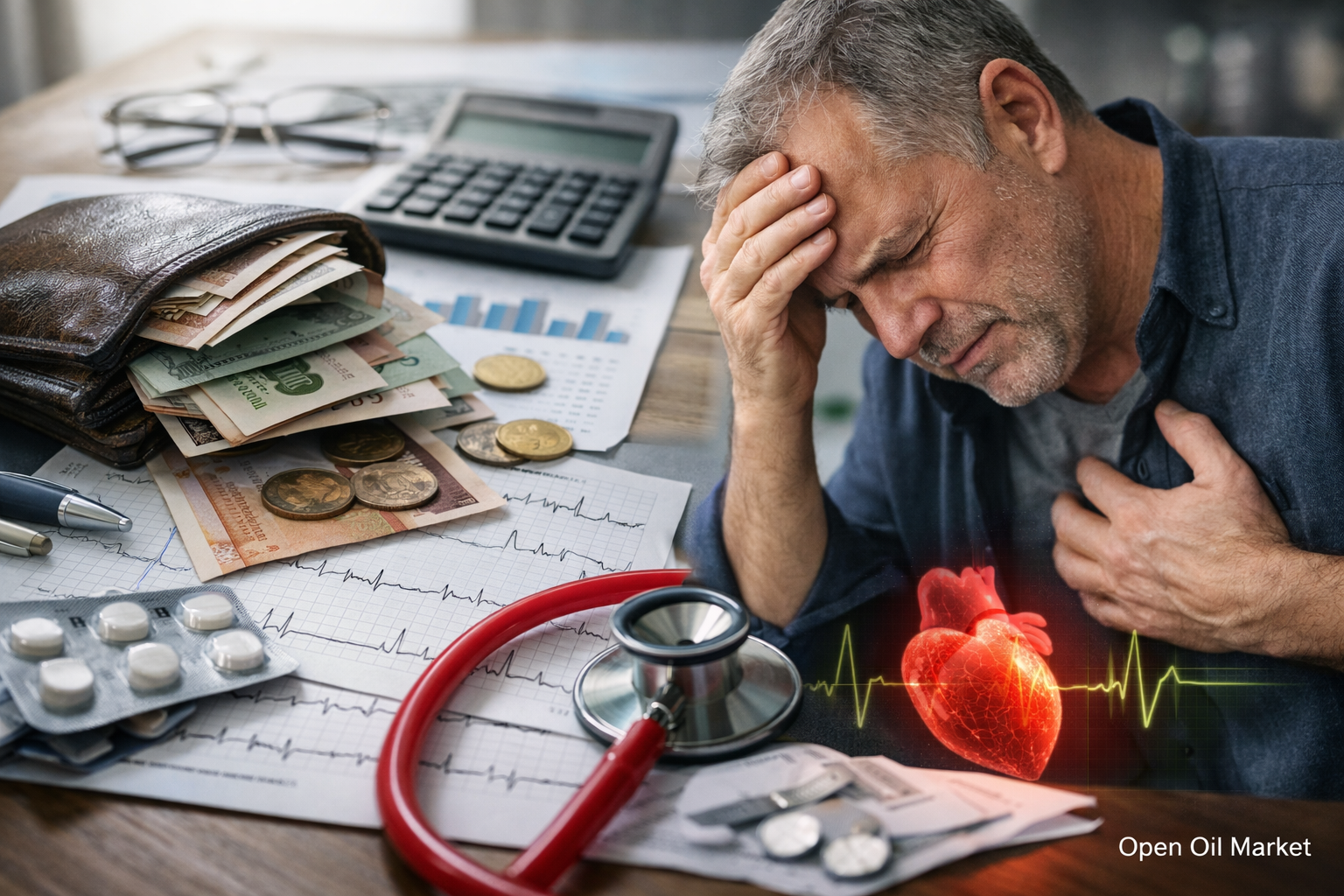

Chronic Financial Stress Accelerates Heart Aging and Raises Mortality Risk More than Heart Attacks: Analyzing Causes, Mechanisms, and Practical Insights for Investors and the Workforce.

Financial instability is rarely perceived as a medical factor. It is often categorized as "life challenges" but not considered a health risk profile. Yet, chronic financial stress—persistent worries about bills, debts, emergency funds, and the next paycheck—acts on the heart not as a singular shock but as a constant burden. For the working population in Russia and Europe, this has become a silent risk multiplier: sleep deteriorates, inflammation rises, blood pressure fluctuates, and habits shift toward quick "anesthetics"—sugar, alcohol, nicotine, and overwork.

A new layer of evidence is being added by technology: artificial intelligence has learned to extract features from ECG readings that correlate with biological age of the heart and likelihood of adverse outcomes. This is critical for investors and managers: heart health is becoming a manageable asset, while financial literacy is evolving into a risk management element, comparable in importance to portfolio diversification.

What's Changed: AI 'Reads' ECGs Deeper than Human Eyes

Electrocardiograms have been a basic test for decades, recording conductivity and rhythm. However, modern machine learning models can identify subtle patterns on ECGs that are statistically connected to the "biological age" of the heart and long-term risks. In public databases assessing "heart age" via AI, it has been noted: if the calculated "heart age" significantly exceeds chronological age, the risk of adverse outcomes (including overall mortality) can be substantially higher—by tens of percentage points, and in some comparisons, around 60% with significant discrepancies.

The key practical takeaway: the heart ages not only due to diabetes or hypertension but also from its environment—including socio-economic pressures and chronic stress.

Poverty and Financial Strain as Risk Factors for Mortality: What Research Says

At the population level, the link between low income, low socio-economic status, and increased cardiovascular mortality is supported by meta-analyses and large cohorts. Generally, low income/education/unstable employment is associated with a higher probability of cardiovascular events and death, even when age and some medical factors are statistically controlled.

A separate line of research specifically examines financial stress: debt burden, income instability, and the inability to meet basic needs. In meta-analyses, financial strain is correlated with an increased risk of major cardiovascular outcomes. For the general audience, this simply translates to: "perpetual lack of money"—is not only about psychology but also about heart health.

Mechanism from Within: How Chronic Stress Accelerates Heart Aging

Chronic stress triggers a chain that resembles "slow wear and tear":

- Heightened Anxiety Hormones: Increased sympathetic nervous system activity raises heart rate and vascular tone.

- Pressure and Heart Rate Variability: Stress worsens blood pressure control and reduces heart rate variability—an indicator of adaptive capacity.

- Inflammation: Stress and sleep deprivation elevate systemic inflammation, accelerating atherosclerosis.

- Behavioral Shifts: Less movement, more "quick calories," increased alcohol/nicotine intake, and late-night eating.

- Deferred Medical Care: Prevention and check-ups are postponed "until better times," which never arrive.

Together, this explains why financial stress can exert a comparable influence to traditional risk factors—especially if it persists for years.

"Alarm Signals" for the Working Population: When to React

Financial stress often masquerades as "normal fatigue." However, there are markers that investors and any managers should pay attention to:

- Consistently elevated blood pressure or "spikes" from minor stressors.

- Shortness of breath during routine activities, reduced endurance.

- Sleep disturbances: late onset, early awakenings, "non-restorative" sleep.

- Increased heart rate, panic episodes, a feeling of "tightness" in the chest.

- Increased stimulant consumption: caffeine, nicotine, energy drinks.

It is important: the goal is not self-diagnosis, but risk management—both in finance and heart health.

Why This Matters to Investors: Health as an Element of Capital Strategy

For an investor, financial discipline is a well-understood tool. However, discipline without resources leads to burnout: an individual maintains risk limits in their portfolio but lives in constant tension. As a result, the likelihood of making "emotion-driven" decisions rises—both in investments and lifestyle choices.

The practical conclusion: financial hygiene reduces not only behavioral risk but also physiological mortality risk. Therefore, "emergency funds," debt management, and cash flow planning are not just about boring accounting but about reducing chronic stress.

30–60–90 Day Plan: How to Reduce Financial Stress Without Illusions

If stress arises from financial concerns, it cannot simply be "meditated away." Managed steps are required:

- First 30 Days: Document cash flow (income/expenses), stop "invisible leaks," set limits on variable spending, compile a list of debts and rates.

- 60 Days: Create a minimal emergency fund (at least 2–4 weeks of expenses), restructure high-interest debts, automate mandatory payments.

- 90 Days: Transition to regular savings (even if small), establish a reserve for 3–6 months, and outline risk management rules (including investments and insurance).

The key terms here are simple: financial literacy, emergency fund, debt control—and less chronic stress for heart health.

Financial Hygiene Tools: A Short Checklist

To reduce financial stress and regain a sense of control, a basic set is sufficient:

- 50/30/20 Budget (or any understandable system): needs, wants, savings.

- One Adjustment Rule: change one expense category per week, rather than "changing everything at once."

- Debt Priority: focus on paying off the most expensive debts first (unless other constraints apply).

- Automated Payments: reduce cognitive load and anxiety from missed payments.

- Reserve Fund: a separate account that is not accessible with "one click."

These steps don't promise wealth, but they diminish the psychological manifestation of poverty—feelings of hopelessness that fuel stress.

"Heart Health" as a Daily Investment: The Minimum That Works

Alongside financial actions, it is crucial to reduce the physiological cost of stress:

- Sleep: 7–8 hours, consistent wake-up time. This is the most undervalued anti-stress tool.

- Movement: 150 minutes of moderate activity per week or 7–10 thousand steps per day.

- Nutrition: less ultra-processed food, more protein and fiber; control late-night snacking.

- Alcohol and Nicotine: not as "stress relievers," but as enhancers of inflammation and sleep issues.

- Prevention: monitoring blood pressure, lipids, glucose, ECG as indicated—better planned rather than emergency care.

The essence of this block for investors: this isn't about "healthy living for ideals," but about reducing the probability of costly events—both medical and financial.

What Companies and Leaders Can Do: Employee Health Economics

Financial stress is a corporate risk: it decreases productivity, increases turnover, and amplifies errors. Effective practices employed in companies across Moscow, St. Petersburg, regions, and international offices include:

- Financial wellness programs: educating about basic financial literacy and debt management.

- Transparent compensation structures and predictable payment schedules.

- Accessible preventive care: blood pressure screening, consultations, corporate check-ups.

- Policies against overwork as a chronic stress factor.

When a company reduces financial uncertainty, it simultaneously reduces chronic stress and improves employees' heart health.

Money Deficiency Is Not a "Personal Weakness," But a Systemic Risk That Can Be Managed

Financial stress is one of the most toxic forms of chronic stress because it is ever-present and seems endless. Research data on social determinants and financial strain indicate: poverty and income instability are associated with higher cardiovascular risks, while modern AI approaches to ECG analysis are increasingly capturing the repercussions of accelerated "heart aging."

For the working population and investors alike, the practical takeaway is clear: reduce financial stress as methodically as you would reduce risks in your portfolio—through emergency funds, disciplined debt management, and controlled habits. This enhances quality of life, decision-making resilience, and ultimately protects heart health.